German Inheritance Tax Allowances (Freibetraege)

Under German inheritance tax law (Erbschaftsteuer), beneficiaries are entitled to tax-free allowances before any inheritance tax applies. These allowances depend on the relationship between the deceased (“decedent”) and the heir.

1. Core Principle

Inheritance tax only applies to the portion of the inheritance above the applicable tax-free allowance. Closely related heirs benefit from the highest exemptions.

2. Personal Tax-Free Allowances

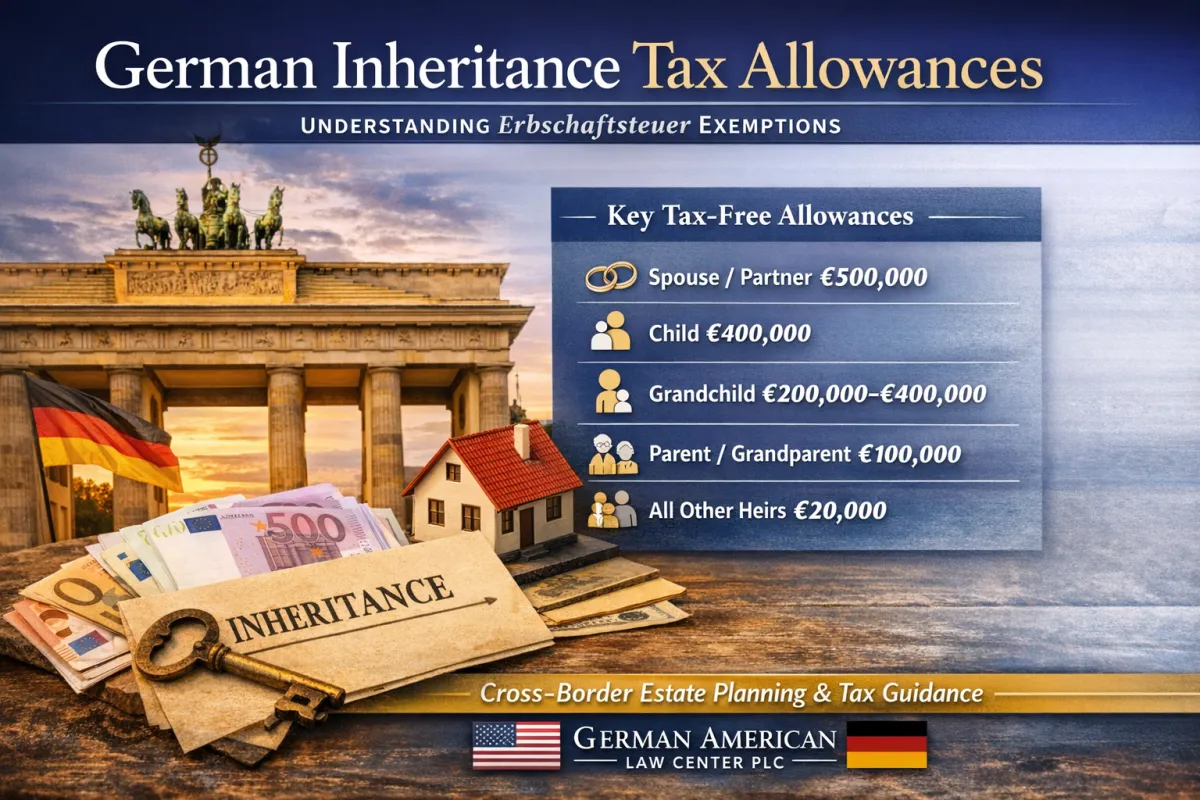

A. Spouses and Registered Partners: €500,000 tax-free allowance. This allowance applies to surviving spouses and registered civil partners.

B. Children: €400,000 tax-free allowance per child. This includes biological children, legally adopted children, and stepchildren (but not foster or godchildren).

C. Grandchildren: €200,000 allowance. If a child of the decedent (the parent of the grandchild) is already deceased, the grandchild’s allowance increases to €400,000.

D. Parents and Grandparents (when inheriting): €100,000 allowance. This applies when parents or grandparents inherit from a descendant.

E. All Other Heirs: €20,000 allowance. This category includes siblings, nieces/nephews, in-laws, former spouses, unrelated individuals, friends, neighbors, and other non-close heirs.

3. Additional Allowances: Versorgungsfreibetrag (Support Allowance)

In certain cases, surviving spouses and children may receive an additional support allowance (Versorgungsfreibetrag). This is designed to support ongoing family maintenance after the loss of a provider.

Spouses: €256,000

Children: A variable allowance based on age (e.g., up to €52,000 for young children, decreasing with age)

This support allowance is reduced if the heir receives a non-taxable survivor benefit (e.g., a pension).

4. Family Home Exemption

Under specific conditions, the family residence can be inherited tax-free by spouses or children:

The heir must move into the home within six months.

The heir must remain living in the home for at least 10 years.

For children, the tax exemption applies up to 200 m² of living space.

If these conditions are not met, the property may become taxable.

5. Other Asset Exemptions

Beyond the main allowances, certain tangible assets may be exempt up to statutory limits:

Household effects and personal items (e.g., furniture, appliances) may be exempt up to a threshold.

For spouses, children, and close relatives, movable property up to a higher value may be tax-free.

For all other heirs, a smaller exemption applies.

(Exact values vary and should be confirmed with current valuation rules.)

6. Practical Considerations

Filing Requirement: All inheritances that exceed the applicable allowance must be reported to the German tax authorities, even if no tax ends up being due.

Planning Opportunities: Gifting assets during life can reset allowances every 10 years, allowing strategic use of exemptions to reduce future inheritance tax.

If you are a U.S. resident or citizen inheriting assets in Germany, professional cross-border legal guidance is essential.

The German American Law Center PLC assists clients with:

German inheritance tax compliance

Certificates of inheritance (Erbschein)

Real estate transfers and sales

Coordination with U.S. tax advisors

End-to-end estate administration in Germany

Schedule a consultation to protect your inheritance and ensure compliance on both sides of the Atlantic.